In hindsight, 2025 stands out for its defining moments that sought to reshape markets and the global economy. From rapid policy and the Federal Reserve’s return to rate cuts to renewed hopes for peace in Europe and the Middle East.

What We Got Right in 2025

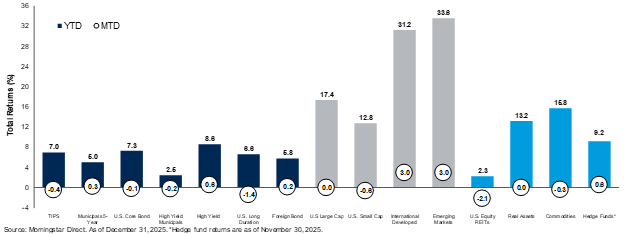

- Fragility in U.S. equities: We anticipated vulnerabilities stemming from full valuations and index concentration. This led us to increase our underweight to U.S. large-cap equities and maintain an overweight to mid- and small-cap stocks, which offered better relative valuations and diversification.

- Global diversification: Our tilt toward international developed and emerging markets paid off, as non-U.S. equities delivered strong performance, reducing concentration risk and enhancing portfolio resilience.

- Fixed income positioning: We emphasized dynamic fixed income and TIPS while eliminating global bonds, positioning portfolios to navigate interest rate volatility and reinflation risk. These allocations provided stability and attractive risk-adjusted returns.

- Alternatives and real assets: Recognizing inflationary pressures and market fragility, we broadened exposure to real assets and advocated for alternatives and private markets. These strategies offered diversification and potential alpha in a challenging environment.

What’s Next for 2026: Themes, Observations, Opportunities, and Risks

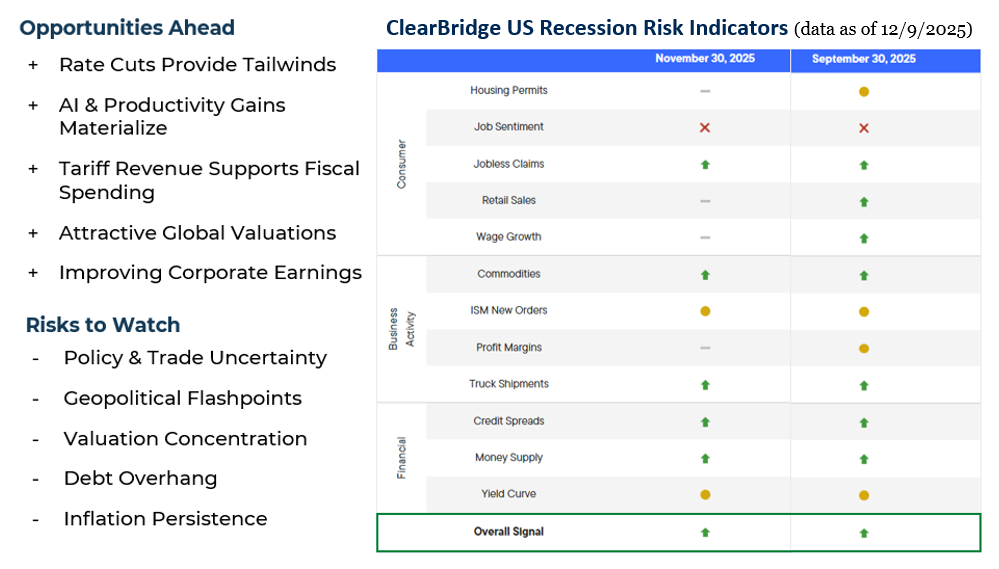

The investment landscape presents a paradox for 2026: compelling opportunities alongside genuine risks. While AI continues to reshape markets, elevated valuations have tempered expected returns. Our 2026 outlook emphasizes disciplined positioning over aggressive moves.

The themes of fragility, durability, and the Age of Alpha proved highly relevant. Most well-constructed portfolios (well diversified, balanced for risk, and aligned with long-term goals) are already well positioned for the year ahead. That means staying the course with modest adjustments, rather than big, dramatic changes. Keep in mind that sometimes, no action is the best action.

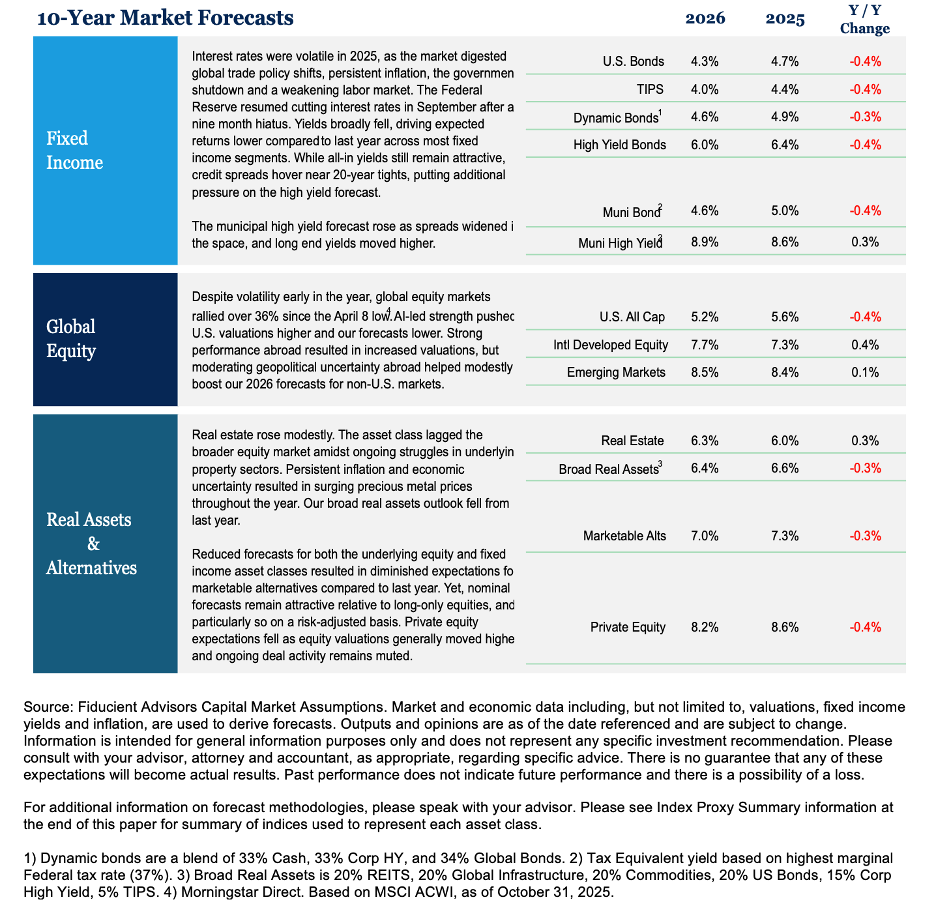

- 2026 capital market assumptions: Most investors point to a tempered outlook as higher valuations and softer yields reduce return potential.

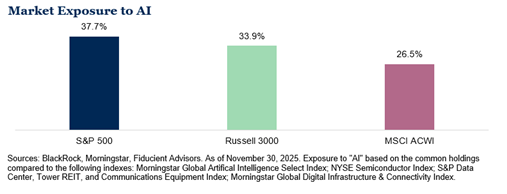

- Artificial Intelligence exposure: Most investors already have significant AI exposure whether they realize it or not. Roughly 38% of the S&P 500 is tied to companies connected to AI, making it one of the most concentrated thematic exposures in market history. The recommended approach is a measured, diversified allocation that balances opportunity and risk, seeking potential upside from AI while hedging against concentration risk.

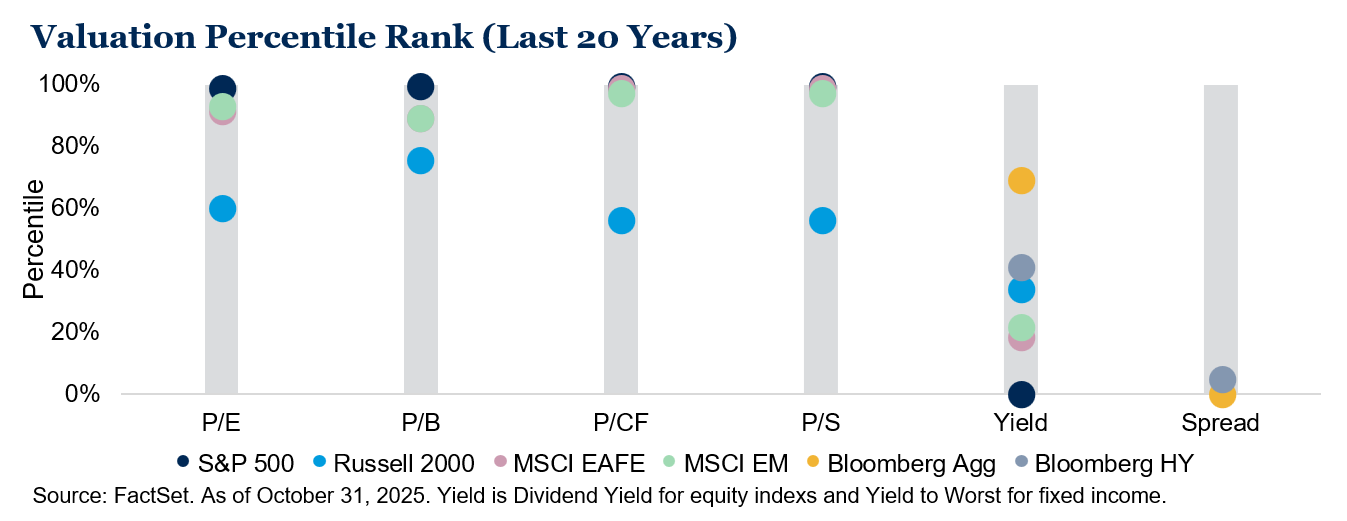

- Elevated valuations shape our positioning: We favor high quality fixed income for risk-adjusted returns, select global equity opportunities and market alternatives to help manage volatility without overhauling portfolios. Most stock and bond markets are trading near 20-year valuation highs. This means long-term returns may be lower than the post-pandemic era. But “full valuations” doesn’t mean “no opportunities.”

- Gradual shifts: The year ahead will likely bring gradual shifts rather than sweeping change. With strong foundations in place, most portfolios need only modest adjustments, underscoring a timeless principle that sometimes, no action is the best action.

The Discipline Dividend in 2026

We enter 2026 with both optimism and realism. Supportive monetary and fiscal policy, a resilient economy, and continued advances in AI provide a constructive backdrop, even as elevated valuations and pockets of exuberance warrant discipline. As stewards of capital, our focus remains on protecting assets rather than speculating. After reviewing market assumptions and portfolio exposures, we see little need for major changes. Modest adjustments and selective use of alternatives may be appropriate, but current positioning reflects a balanced approach to risk and opportunity.

Four Principles for Staying Disciplined in 2026

- Don’t panic or overreact: Market volatility is normal. Avoid overreacting to short-term events.

- Rebalance, don’t overhaul: Keep allocations near your targets, use incremental adjustments, and consider tax-efficient moves.

- Consider alternatives selectively: Modest exposure to alternatives can help diversify risk, but suitability depends on your individual situation.

- Stick with quality and diversification: Focus on well-capitalized stocks, investment-grade bonds, geographic diversification, and consider discussing active management with your advisor where appropriate.

Contact your advisor to discuss your portfolio positioning for 2026. You can set up a wealth alignment call with Wealth Sync Partners by clicking here.

Sources

- https://www.fiducientadvisors.com/research/2026-outlook-the-discipline-dividend

- https://www.fiducientadvisors.com/research/december-2025-market-recap

- https://www.fiducientadvisors.com/research/2025-fourth-quarter-considerations

Disclosures and Index Proxies

This report does not represent a specific investment recommendation. Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and are reported gross of any fees and expenses. Any forecasts represent future expectations and actual returns; volatilities and correlations will differ from forecasts.

When referencing asset class returns or statistics, the following indices are used to represent those asset classes, unless otherwise notes. Each index is unmanaged, and investors can not actually invest directly into an index:

“Finding the Right Balance” global equity allocation top 10 weights based on the following weighted average portfolio of indexes: S&P 500 (41.8%), Russell Mid Cap (12.5%), Russell 2000 (8.2%), MSCI EAFE (26.1%) and MSCI EM (11.5%).

Material Risks Disclosures

Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

Cash may be subject to the loss of principal and over longer period of time may lose purchasing power due to inflation.

Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impact by currency and/or country specific risks which may result in lower liquidity in some markets.

Real Assets can be volatile and may include asset segments that may have greater volatility than investment in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disaster.

Private Equity involves higher risk and is suitable only for sophisticated investors. Along with traditional equity market risks, private equity investments are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility and/or the potential loss of capital.

Private Credit involves higher risk and is suitable only for sophisticated investors. These assets are subject to interest rate risks, the risk of default and limited liquidity. U.S. investors exposed to non-U.S. private credit may also be subject to currency risk and fluctuations.

Private Real Estate involves higher risk and is suitable only for sophisticated investors. Real estate assets can be volatile and may include unique risks to the asset class like leverage and/or industry, sector or geographical concentration. Declines in real estate value may take place for a number of reasons including, but are not limited to economic conditions, change in condition of the underlying property or defaults by the borrow.

Marketable Alternatives involves higher risk and is suitable only for sophisticated investors. Along with traditional market risks, marketable alternatives are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility or the potential for loss of capital. Additionally, short selling involved certain risks including, but not limited to additional costs, and the potential for unlimited loss on certain short sale positions.